Shaping the luxury menswear market

Enhance your menswear strategy with Retviews

Stay ahead of the curve with Retviews

Find out how our competitive intelligence platform enables brands to monitor competitor strategies in real-time and adapt their own collection accordingly, avoiding guesswork and remaining ahead of the curve. Retviews, the AI-powered benchmarking platform, enables your company to enhance its assortment strategy and establish the best pricing strategy, reducing time spent on manual benchmarking.

Key takeaways

- The menswear market is witnessing an “unprecedented” boom, fueled by a fashion reset.

- With Retviews, it is possible to get the right pricing strategy for each country and increase profits, while analyzing your price positioning per category.

- Luxury brands are lacking in extended size ranges for menswear, filling this gap could be a key factor in boosting a brand's performance.

The menswear apparel market is experiencing an unprecedented boom. According to Euromonitor, global menswear sales are expected to reach $547.9 billion by 2026, with the apparel market valued at $60 billion in 2021, in the US only. With the menswear market growing at a faster annual rate than womenswear, luxury brands are currently seizing this opportunity and increasing investments in menswear.

As the current situation is characterized by unpredictability, due to price inflation, supply-chain disruption and changing consumer preferences, find out how Retviews can help your brand nail your menswear collection and stay ahead in this growing market.

Focusing on accessories and leather goods

Retviews’ data have previously outlined how the global pandemic led to a reset in the male dress code, with a reduction in formal attire and a shift towards smarter casual wear, leading to the demise of ties and a rise in casual suits. Automated competitive analysis platform Retviews makes it possible to analyze leading brand assortments, spot different strategies and identify new opportunities.

One main difference between accessible luxury brands and their high-end counterparts is the share of leather goods in their assortment – usually one of the predominant categories for high-end brands. Retviews’ data show that luxury leaders Saint Laurent and Louis Vuitton are among the brands with the biggest focus on leather goods, which make up 30% and 28% of their assortments, respectively. On the other hand, only 19% of Gucci’s menswear assortment is made up of leather goods, as accessories take the lead.

Burberry’s higher up-market move is also evident within its menswear assortment, as it has a larger share of leather goods than accessible luxury brand Armani. Wanting to move closer to high-end luxury, Burberry’s assortment reflects the high-end prominence of leather goods.

The high-end luxury menswear market maintains a stronger focus on accessories and leather goods than ready-to-wear. On the other hand, accessible luxury brands have a strong assortment share of ready-to-wear categories such as tops and bottoms, with a smaller collection of leather goods.

There is a major focus on sneakers rather than formal shoes, within leading brands’ menswear assortments. This is partially attributed to Louis Vuitton and Gucci tapping into streetwear and activewear, through recent collaborations with Supreme and Adidas. However, sneakers are losing ground to loafers, which are one of the most popular shoe styles of 2022, recording a +54% YoY increase in leading brand assortments, according to Retviews. Accessories has also become a growth category over the last year, with a strong increase in demand for sunglasses, bags and jewelry.

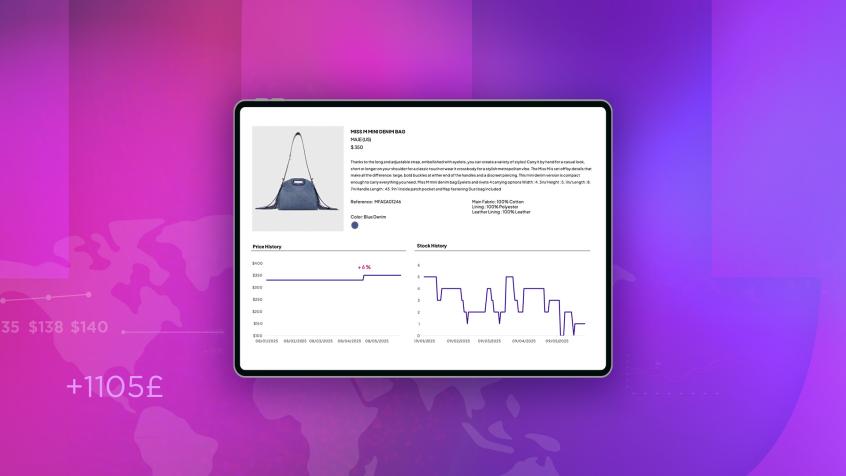

As indicated in the graph above, there has been a +9% YoY increase in bags within leading brand assortments, with cross-body bags being the most prominent style in the assortment, seeing a +38% YoY increase.

When targeting luxury menswear, it is essential to know exactly how to position your offer on the market, with the right product mix that will resonate with respective consumers. Thanks to Retviews’ real-time data, luxury leaders are monitoring their competitors’ assortments and pricing strategies, and getting the most relevant collections, at the right price and time.

Achieving the right price structure

When it comes to benchmarking, brands’ purchasing teams monitor pricing structure per category, to make sure that their brand is aligned with competitors, in terms of pricing strategies. Retviews makes it possible to save time on manual benchmarking thanks to its accurate, real-time data.

Burberry has recently been trying to elevate its offer, however, as Retviews data show, its outerwear and suit ranges still have lower prices than accessible luxury brand Armani. This could indicate an opportunity for the UK luxury leader to reposition its prices for the two categories in its upmarket move. Retviews enables brands to get an in-depth view of their pricing strategy compared to their competitors’ and spot opportunities for improvement, boosting revenues.

Luxury brands’ international pricing strategies

For brands’ purchasing and merchandising teams, developing an international pricing strategy is a challenge, seeing as markets are subject to change. With Retviews, your brand will be able to see your competitors’ strategies to draw comparisons and improve positioning.

As shown by the data, high-end luxury players all maintain a higher price point in China, compared to the US. Accessible luxury brand Armani, however, has a lower price within the Chinese market. The brand could increase prices within China and optimize revenue. Armani also has the strongest price difference between markets, as the Chinese, UK, French and Italian markets all have a lower average price point than the US market.

Could this be an accessible luxury strategy or does Armani have significant room for improvement? With access to Retviews’ real-time data, your brand can pinpoint the ideal positioning for your collection, on an international scale.

Size inclusivity in menswear: a major shortage

The US plus-size men's apparel market was worth 848.9 million dollars in 2021, and its value is expanding twice as quickly as overall apparel sales in the United States. From a business standpoint, this represents a tremendous opportunity for companies. The luxury industry is known for lacking inclusivity, especially for menswear.

Retviews data show that Burberry and Prada are the only brands offering a wider range of sizes, with Burberry stocking size 3XS and Prada’s offer reaching 4XL. A lack of inclusive sizing results in brands missing out on a wider range of potential consumers.

With Retviews, it is possible to confidently build a size inclusive collection, as the platform allows your brand to spot where your assortment is lacking or spot gaps in your competitors’ assortments and find potential opportunities for your own collection. Retviews helps your brand not only analyze the size assortment of your competitors, but also compare how their strategy differs between countries and even by style of a specific product.

Delving deeper into Retviews data showed that each luxury leader’s assortment differs by country. Burberry and Prada have a wider size range for their US assortment, whilst Armani has a wider size range in the UK. On the other hand, both Celine and Gucci have larger assortments in China. This is a strategic move for Gucci, where the Chinese market provides more than half the brand’s total revenue.

With a 360° overview of competitors’ size structures, your brand will be able to avoid the guesswork of manual benchmarking and nail your size inclusive collection.

Retviews, the AI powered benchmarking platform for every role in the fashion industry

By adopting Retviews’ tools in their daily tasks, purchasing, merchandising, product, and digital teams will be more efficient and save significant amounts of time on manual benchmarking, by accessing data in real-time. Retviews’ data will allow your brand’s teams to be proactive towards the fashion industry’s ever-evolving dynamics and adapt their strategies with ease.

Use the Retviews platform to benchmark your offer against your competitors

Related Content